With examples that can help you prepare for your circumstances

The LTA tax charge applies when a BCE occurs and the value ascribed to that BCE exceeds your remaining lifetime allowance.

If you have taken pension benefits in the past and therefore experienced a BCE, then you will have used some of your LTA. This is calculated as the percentage of the LTA, at that time, that was utilised.

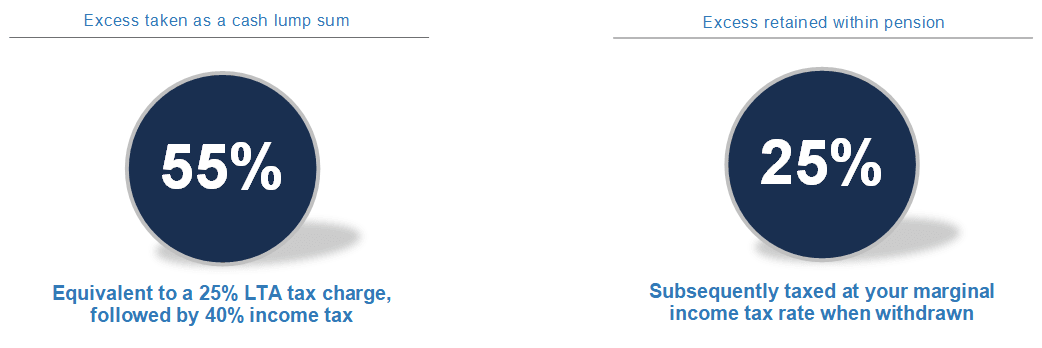

With a defined contribution, also known as a ‘Money Purchase’ pension, it is the sum that exceeds the LTA that is taxed and the level of this tax depends on whether the excess is paid out to you as cash or retained within the pension wrapper.

If you have a defined benefit, also known as a ‘Final Salary’ pension, then the lifetime allowance tax charge is calculated in a similar way to the above. However, how it affects the pension you end up receiving will also depend on your specific pension scheme. If your defined benefit entitlement exceeds the LTA, some schemes give you the option of either taking the excess as a lump sum, subject to the 55% tax charge, or taking a reduced annual pension. However only one of these two options may be available.

If the defined benefit pension scheme does allow you to take a reduced annual pension, then the amount your pension reduces by also depends on the scheme’s specific rules. This is because although the tax charge is the same in each case at 25% of the excess, different schemes use different commutation factors to work out how much effect this tax charge has on the annual pension you receive.

If in the 2022/2023 tax year someone aged 65 crystallised a defined contribution pension worth £1,500,000, they would have exceeded the lifetime allowance by £426,900 (£1,500,000 minus the current LTA of £1,073,100).

Of the £1,073,100 within the LTA, 25% (£268,275) may be taken as a tax-free lump sum. The remaining 75% (£804,825) can stay in the pension for withdrawal at a later date, subject to income tax.

Of the £426,900 that exceeds the LTA, the investor may choose to either receive an additional cash lump sum of £192,105 (£426,900 minus a 55% tax charge), or an additional £320,175 that remains in the pension (£426,900 minus a 25% tax charge) and will be subject to income tax when withdrawn.

Taking this example further we can consider what would happen when the person reaches age 75. At age 75, the funds remaining in the pension are compared to value in the pension after it was crystallised. If the excess was taken as a cash lump sum then £804,825 would have remained in the pension. If the pension is worth anymore than this figure at age 75 then a 25% tax charge applies to the excess.

Between first crystallising the pension and reaching age 75 the investor is able to withdraw any growth from the pension to ensure that they do not exceed the threshold and become liable to a further LTA tax charge. Whether this is worth doing or not depends on various factors, as we shall look at in more detail in the next section. The video below may also help you to plan ahead better and efficiently manage your investments.