How to manage your lifetime allowance

Some people with larger pensions will potentially face additional charges in the form of the lifetime allowance (LTA). This is applied when the value of your pension exceeds £1,073,100, a level frozen until 2026.

The lifetime allowance was first introduced in 2006 at £1.5m, after which it increased each year before being reduced between 2012 and 2016. Various levels of Fixed Protection have been available to investors over these years, protecting the level of the LTA in return for certain restrictions such as no further pension contributions.

If you have not added to your pension savings since 5 April 2016 you may still be able to apply for Fixed Protection 2016, which will give you a personal lifetime allowance figure of £1,250,000.

You are able to check your existing protection using your Government Gateway user ID. If you do not have a user ID, you can create one when you check.

• As pension savings grow, more and more people are affected by the LTA

• Investors do have choices and you can plan for its impact in advance

• The right guidance helps to make the most of any mitigation opportunities

• The LTA is complex so this article might provide some helpful pointers and also links to our useful lifetime allowance calculator to help you evaluate how much of an LTA tax charge you might incur

The LTA Tax Charge

The LTA tax charge applies when a benefit crystallisation event (BCE) occurs - where the value of your pension is assessed - and the value ascribed to that BCE exceeds your remaining lifetime allowance.

If you have taken pension benefits in the past and therefore experienced a BCE, then you will have used some of your LTA. This is calculated as the percentage of the LTA, at that time, that was utilised.

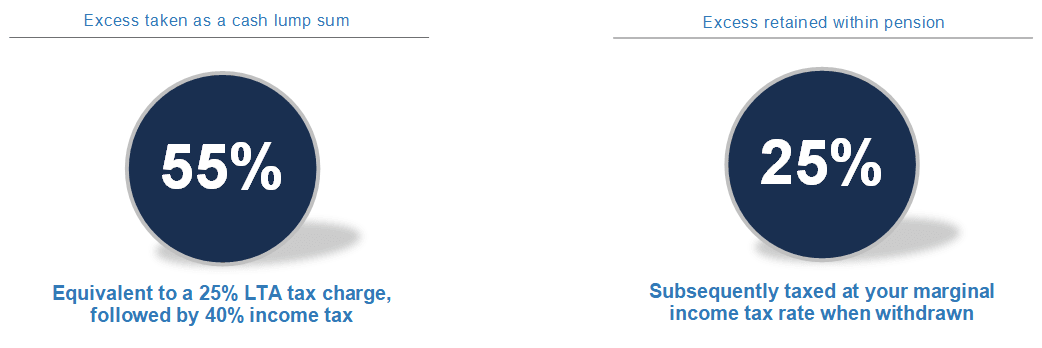

With a defined contribution, also known as a ‘Money Purchase’ pension, it is the sum that exceeds the LTA that is taxed and the level of this tax depends on whether the excess is paid out to you as cash or retained within the pension wrapper.

If you have a defined benefit, also known as a ‘Final Salary’ pension, then the lifetime allowance tax charge is calculated in a similar way to the above. However, how it affects the pension you end up receiving will also depend on your specific pension scheme. If your defined benefit entitlement exceeds the LTA, some schemes give you the option of either taking the excess as a lump sum, subject to the 55% tax charge, or taking a reduced annual pension, however only one of these two options may be available.

If the defined benefit pension scheme does allow you to take a reduced annual pension, then the amount your pension reduces by also depends on the scheme’s specific rules. This is because although the tax charge is the same in each case at 25% of the excess, different schemes use different commutation factors to work out how much effect this tax charge has on the annual pension you receive.

For specific advice about your potential LTA situation, our team of qualified advisers can help you to explore the possibilities. Book a call with them here.