And learn how to pay for them

Your future goals may involve the spice of adventure and the excitement of trying new things. Yet you should also balance these personal objectives with the reality of how to pay for changes in your life. Your income structure might be different, for example, if you don’t have a salary – will your new retirement income cover the things you want and need?

You may wish to travel more, take up new hobbies or give to loved ones. Setting clear financial goals gives you a greater sense of control and helps you to effectively meet your objectives.

You should also think about the structure of your assets and how various accounts fund different goals. For example, a pension is ideal to grow your assets over time and generate tax-free cash, while you may have funds in a general account which are taxed but easily accessible. An ISA is tax free but within your estate and you might consider too about releasing value from a property to give you more freedom.

Carefully managing the interplay of these accounts will help you maximise the assets you have, but it can get complex, so it may be worth talking to an expert about your options.

When you do retire, you have two main options to fund your retirement: an annuity or a flexible access drawdown. Both have benefits and points to consider, depending on your circumstances and preferences.

You should consider how long your pension pot could last and understand where the trade-offs are. For example, would you like to give up some potential income for more certainty by taking less investment risk or buying an annuity?

Make time work for you – by setting your time horizon

Achieving your goals is explicitly linked to your time horizon – how long before your retirement and for how long a retirement do you wish to plan for. The longer the time you can invest, the more risk (with potentially higher returns as a result) you can take to realise these goals.

A reasonable timeframe allows you to take on more market risk because the potential for volatile outcomes, particularly negative outcomes, is reduced and typically outweighed by positive outcomes over a period. Shorter periods, such as a year, are much more likely to be volatile and increase the chance of lower returns.

By looking at the potential outcome for our Risk Level 2, 4 and 7 portfolios, we can see how a longer timeframe can accommodate more investment risk.

So while it is important to think about your time until retirement, you should also consider how long you may live after you do retire. This is easy to underestimate, but people are typically living longer, and if you take early retirement you should ensure you can afford to pay for those extra years.

Source: Bloomberg and Netwealth. Percentage number of total periods a negative return would have occurred for an investment over the relevant time period. Monthly data from the beginning of 1996 to end of 2021, based on example asset allocations for Netwealth Risk Level 2, 4 and 7 portfolios.

Risk vs reward: decide how much risk you should take

It’s important to address some of the negative associations that arise around taking risk. Because risk shouldn’t be viewed as having the binary outcomes of either making or losing money – but rather how much you could gain or lose over a certain period.

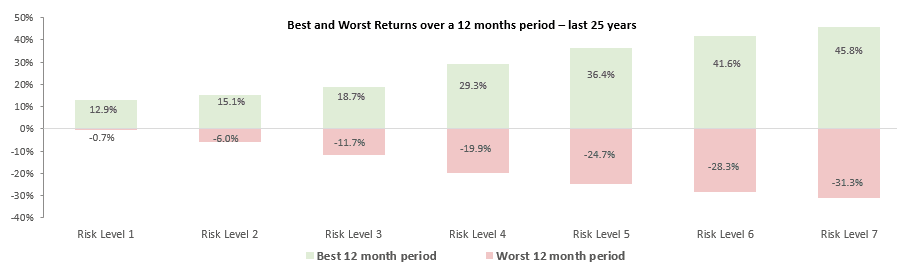

Longer timeframes give you the best chance of a more favourable outcome, as we have shown. That said, you should be aware of the real implications of taking risk – both from a positive and negative standpoint. Let’s take a look at the seven different risk levels we offer at Netwealth to illustrate the best and worst returns for each risk level over the last 25 years.

These give you an idea of the extremes you could face.

Source: Netwealth. Based on example asset allocations for Netwealth 1-7 Risk Level portfolios for the 25-year period to the end of 2020. Simulated historic performance is not a reliable guide to future performance.

You should also note that these figures are extreme 12-month plus or minus figures. Few years have these swings, and the chart does not take into account the rewards of taking higher risks over time, and the compounding of these returns which add up considerably.

The concept of risk is also worth thinking about in these different ways to give you a fuller understanding of its impact: